2024 Investment Letter

Welcome to our fourth annual investment letter.

In 2024 we both successfully transitioned into having our own (separate) businesses. Claire co-founded Haylo Ventures, a deep-tech venture operator. While Amir acquired Saepio and started working as it’s Co-CEO. This reduced the amount of time we had to source deals to 0, regardless we did continue to angel invest during 2024.

In this year’s letter we will cover the following topics:

Deal-flow

Investment Philosophy

LP Investments

New Angel Investments

Portfolio funding rounds

Howbout that

Profitability is back in fashion

The bad stuff

Selling our pro-rata

1) Deal-flow

Deal-flow has been a consistent theme in our letters. Due to the change in our professional lives, we decided to stop outreach as a whole and only look at inbound deals. So we turned off the contact page on our website and removed any links to our airtable. In effect creating a test to only find the most persistent of founders. This in turn led to a big shift in sources of deal-flow:

Co-investors in previous investments. This became our primary source for dealflow and we felt it was a high quality source. As such, this is a source we will continue to encourage by proactively sharing any deals we are investing in or think are interesting.

VCs. We continued to get leads from VCs who felt the leads were too early for them, but of quality. However it is clear that our description of pre-seed is a lot earlier than a VCs and these deals feel more like seed deals!

Inbound from LinkedIn. This is how Firenze found us but outside of that, this was a low quality source in the funnel.

2) Investment Philosophy

Our 4 core principles did not change in 2024, however as our purse strings tightened, so did our discipline in not making exceptions to our principles!

Is the problem in an area we understand, can evaluate and (potentially) add value to?

Is the problem described a real one that needs to be solved?

Is the solution being pitched a possible and likely solution to the problem?

Is the founding team capable of executing on the solution and do we think we can work harmoniously with them to help them?

#4 continued to be the most important factor in our decision making.

3) LP Investments

This year we expanded investing as LPs by making 2 investments.

First we re-invested into Outward VC and their Fund II. We are happy with how Fund I’s portfolio is performing, we believe in their investment thesis, the rigour they apply and have a symbiotic relationship where they help us with angel screening and we provide deal-flow. In January 2025 we hope to see Outward lead the seed round of one our pre-seed investments. A very exciting first, we are looking forward to!

Additionally we invested into our first consumer fund by becoming LP’s in the Sidemen’s fund: Upside. We have been working with the Sidemen’s investment team for 18 months now, leading to them co-investing in Howbout and GlobalComix. The Sidemen team have also personally invested in some of the earlier stage investments (PTB) in our portfolio. We have a similar symbiotic relationship here to our Outward relationship.

In summary our goal is to uncover and mentor very early stage startups in the consumer to fintech space. Help them put together angel led rounds, grow to early signs of meaningful size and then hand them over to VC funds that we work closely with and trust.

4) New Investments

In 2024 we saw a shift from the previous year’s focus on consumer investments to seeing a heavy weighting on FinTech investments. This was market-led and unexpected, as in previous years we felt early stage FinTech investments were severly over-valued and we saw a large correction in 2024.

In total, we ended up doing 5 investments and 3 follow-ons (CreatorOS, Howbout and Quiver) in 2024.

Higgsfield AI

Our first investment of 2024 was meant to be our last investment of 2023 but due to a few issues with the SWIFT payment details, the funding got delayed by a few days and slipped into 2024!

We became aware of Higgsfield when Claire’s former Snap colleague Alex contacted Claire about his new foundational LLM start-up. Alex joined Snap in 2020 and became the director of generative AI when they bought his startup AI Factory for $166m. This then became the Snap’s generative AI engine. Post investment it was great to see Akin would also be joining us on the cap table, making this our 2nd co-investment with him.

Firenze

Additionally, early in 2024 Amir recieved a LinkedIn message from David Newman, someone he had never met. David was pitching his new startup Firenze cold and had reached out after seeing a LinkedIn post about our investment into SooperBooks and them featuring on BBC’s Dragons Den.

After grilling David a few times in back and forth LinkedIn messages, Amir organised a call and asked co-investor Andi to attend too. Amir happened to be resarching Lombard loans at time for personal reasons and Andi had previously worked in a private bank. As such both were familiar enough with Lombard loans to be able drill into the topic.

After jumping on the call, it took about 5 minutes for both to want to invest. After agreeing with David that it was best to keep it as an angel only pre-seed round, Amir and Andi set about trying to help David raise £750k in this way! Each introduction made, led to those angels investing and introducing others and very quickly the Fintech super-angel round was complete.

Ontime (formerly PayLo)

The 3rd investment of 2024 was in April. Ontime is a new startup led by Miles Hance-Lambie, previously the CPO of Salary Finance, giving him the perfect experience to launch a start-up focused on paying scheduled bills (like utilities) through payroll. Miles is joined by Frank Sedivy and Simon Cockle.

We were introduced to Miles by the fabulous Alex Cardona (of Codat fame). There is a separate angry rant needed about Alex not letting us invest in his new startup Recorder, but that’s for another time! :)

Amir had the pleasure of sitting next to Alex at a Hedosphia Fintech investor dinner and they realised they have a lot of friends in common and from that started exchanging dealflow. Amir sent Alex ‘Firenze’ and in return Alex sent Amir ‘PayLo’ which became Ontime.

ComplyStream

September brought the 4th investment of the year with ComplyStream. Amir has been a member of the ‘FinTech Product Guild whatsapp group’ for a few years now and another early member was Kartik. Upon launching his startup, Kartik contacted Amir on whatsapp and asked if he could pitch his new idea.

Similarly to Firenze, Amir liked the idea, agreed to invest and also agreed to help put the angel round together to fund it. After quickly wrapping up a £250k friends and family round, Kartik was approached by the early stage funds; Cornerstone and Ascension who also wanted to invest. As such the round valuation was slightly raised and it was converted into a pre-seed round.

Curve

We were originally not going to include this investment as it’s not an early stage angel ticket but for completeness we did also invest in a convertible note in Curve.

5) Portfolio funding rounds

As you would expect after 5 years of investing, we are starting to see some performance divergence in our portfolio. Of particular interest to us has been observing which start-ups have been able to raise new funding rounds based on their performance.

Series A continued

After the success of Lapse being our first pre-seed to Series A in late 2023, We saw Howbout join the Series A club too. We expect this to accelerate in 2025, as a number of our investments have already done pre-Series A SAFEs/ASAs.

So, as things stand we have 2 out of 22 pre-seed tech investments at Series A. We can comfortably see at least 3 more Series As in 2025. We don’t know if 2 out of 22, let alone 5 out of 22 for Pre-seed to Series A is a good ratio or not, but we are happy with it. Well as happy as you can be when you haven’t actually sold your stakes and cashed out!

2023 Dec - Lapse Series A led by Greylock and DST

2024 Sept - Howbout completed Series A led by Goodwater

Other notable raises

2023 YE /2024 Jan - Yurtle raise a seed round led by InsureTech Gateway.

2024 April - Algbra completed a late seed convertible led by SCV.

2024 April - Higgsfield completed a late seed SAFE led by Menlo Ventures.

2024 Nov - GlobalComix completed a late seed SAFE led by Point72.

2024 Nov - ID Wise complete an institutional-style late seed ASA led by a prominent family office.

Note: There was going to be one more raise (Angel Pre-Seed to VC led Seed in less than 6 months) included in the list here, but last minute ‘legals’ dragged the deal into January 2025.

6) Howbout that?

Words cant convey quite how happy we were to see our first ever investment Howbout, get to Series A. Never have a set of founders deserved it more. It was even more exciting to see Goodwater leading the round, a firm who impressed all the existing investors in the sheer amount of DD they did and the level of benchamrking data they were able to show in the consumer space. They have continued this rigour post-investment too!

The story of Howbout is an incredible one of perservence and our faith in the team has not wavered. As a reminder:

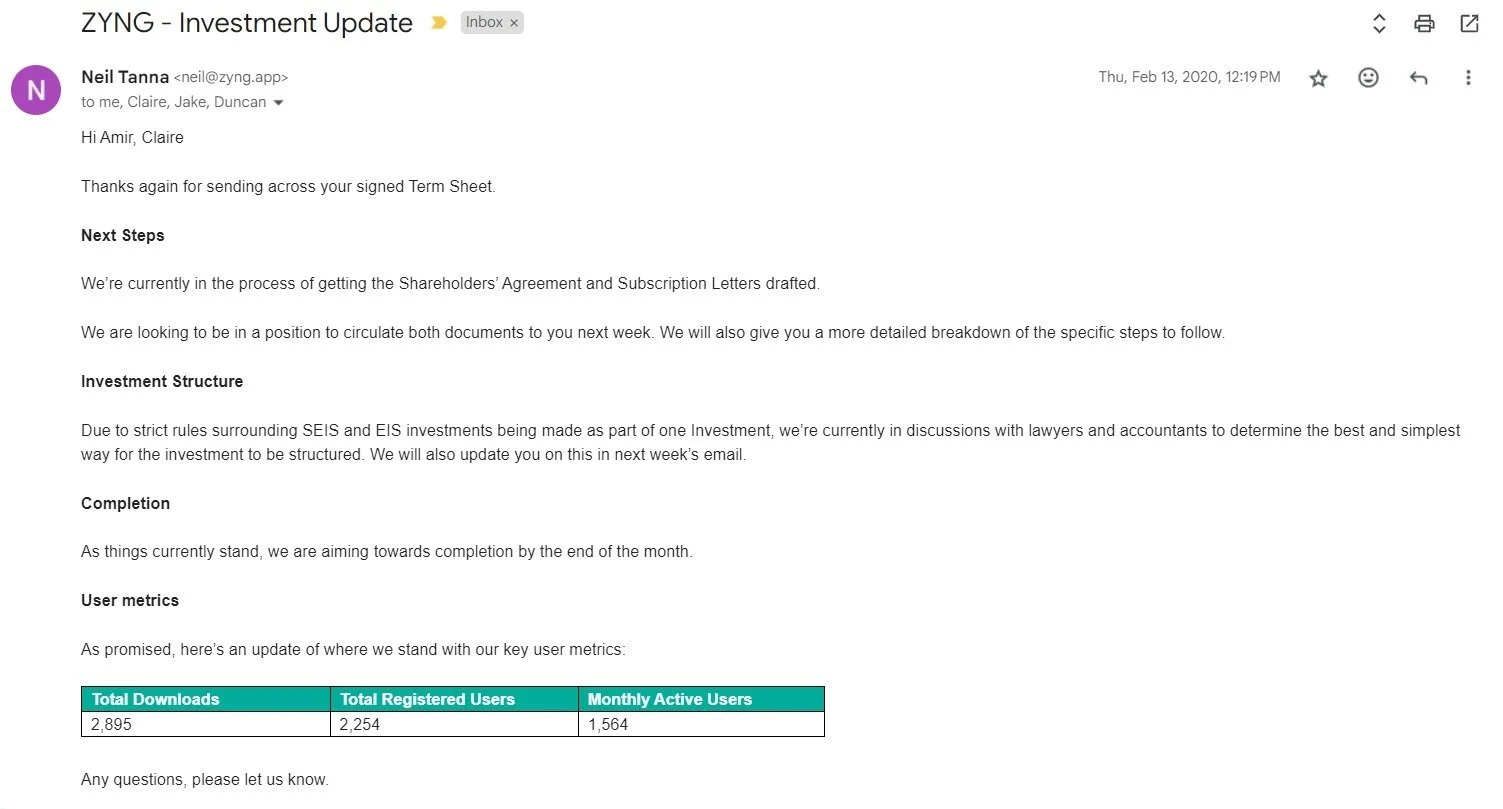

2020 Jan - The boys pitch to us a social calendar (called ZYNG) which we agree to do the pre-seed for.

2020 Feb - Two weeks before term sheet signing, global COVID lockdowns kick-in (Feb 2020) and there is no socialising, but we still do the round:

2021 March - Now called Howbout the app keeps launching between lockdowns and showing very promising engagement and network effect data but people are still not socialising. We still do a round.

2022 Nov - Through the 4 lockdowns in the UK, the app has collected enough data to convince a few funds that there is definitely something there but it just needs a bit more continuous time of socialising to prove it! Another round is done.

Truly a journey for the ages!

As things stand, we think the Howbout team are building the next big consumer app and this is shown in their engagement and retention data, alongside their network effects driven virality. From 2k users to 4m, its been a hell of a ride!

P.S. Congrats to the team for closing the round a week before Neil’s wedding!

7) Profitability is back in fashion

As the fundraising climate has corrected away from speculative investments, we saw some founders shift their priorities to making their startups sustainable and profitable:

CreatorOS - The team built a managed SaaS solution for agencies that has been pretty much profitable from Day 1. Due to the lumpy (large) nature of some of the contracts they win from media agencies, the level of profitability is variable.

Konvi - Konvi has been showing profitable months since 2023, with 2024 showing a consistent / sustainable monthly profit. As such, the team are focused on growth / acceleration and any future fund raising they do, would be solely focused on this too.

ID Wise - Being the first true AI powered IDV solution allowed ID Wise to have far superior unit econimics. This translated into their all-ARR business growing into a Q4 2024 that was EBITDA proftiable.

Homefans - Having a business tied into sports calendars has always given a cyclical quality to Homefans earnings, with active months being profitable throughout 2024. By launching European sports events alongside the existing South American events, 2025 should see all year round profitability.

8) The Bad Stuff

In last year’s letter we wrote about our first investment (Aisle 3) going into liquidation and Aura Fertility having a nominal ‘acqusition’. 2024 saw the founder of Bunsen close the marketplace down due to not believing in the TAM size (and not wanting to waste time). We then saw the founder of FROW shutter it into zombie mode.

So at this stage from 22 early stage tech investments (i.e. exlcuding Curve):

2 to Series A

3 shuttered

1 ‘acquired’

Statistically, these results are to be expected, so nothing to worry about but they have created a red flag for us in our investment thesis. We will not invest in a founder that struggles to raise money (this is proving to be a sign of future repeat pain) and/or has a very unproven TAM for the market they are entering.

9) Selling our pro-rata

In 2024 we tried a new experiment where we offered family offices a portion of our premption pro-rata allocation under the terms of a bare trust.

I.e. Our names would remain on the cap table, we would fund the startup from our account but part or all of the investment would be funded by a SFO/MFO, who under the terms of a bare trust would own the tax obligations and slightly less than 100% (i.e. minus our fee) of the allocation they funded.

We were able to do this for the Series A investment into Howbout for half our allocation (we funded the rest) and plan to explore this option everytime going forward where our allocation is £100k+, rather than waiving our premeption pro-rata rights.

At the moment we are doing this without charging carry and purely an upfront allocation fee.

PS

As always we use AI to create an image for our annual investment letter. This year’s image was generated by Microsoft Designer.

The prompt used was: ‘A married couple who angel invest in tech companies. The husband is very handsome 45 year old bald iranian with a beard. His hair colour is black. The women is a very attractive brunette Italian lady. The setting is inside a high tech office with lots of money sitting on the floor.

If you go through the images for each of our annual investment letters, it’s a really good tracker of AI progress!